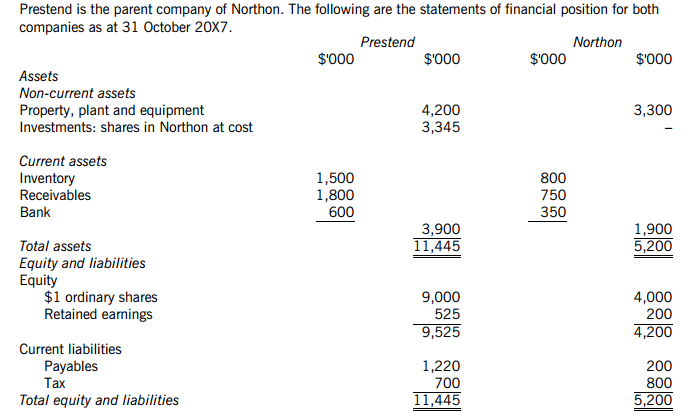

You are presented with the following trial balance of Malright, a limited liability company, at 31 October 20X7.

Dr Cr

$'000 $'000

Buildings at cost 740

Buildings, accumulated depreciation, 1 November 20X6 60

Plant at cost 220

Plant, accumulated depreciation, 1 November 20X6 110

Land at cost 235

Bank balance 50

Revenue 1,800

Purchases 1,105

Discounts received 90

Returns inwards 35

Wages 180

Energy expenses 105

Inventory at 1 November 20X6 160

Trade payables 250

Trade receivables 320

Administrative expenses 80

Allowance for receivables, at 1 November 20X6 10

Directors' remuneration 70

Retained earnings at 1 November 20X6 130

10% loan notes 50

Dividend paid 30

$1 ordinary shares 650

Share premium account 80

3,280 3,280

Additional information as at 31 October 20X7:

(a) Closing inventory has been counted and is valued at $75,000.

(b) The items listed below should be apportioned as indicated.

Cost of Distribution Administrative

sales costs expenses

% % %

Discounts received -- -- 100

Energy expenses 40 20 40

Wages 40 25 35

Directors' remuneration -- -- 100

(c) An invoice of $15,000 for energy expenses for October 20X7 has not been received.

(d) Loan note interest has not been paid for the year.

(e) The allowance for receivables is to be increased to the equivalent of 5% of trade receivables. Anyexpenses connected with receivables should be charged to administrative expenses.

(f) Plant is depreciated at 20% per annum using the reducing balance method. The entire charge is to be allocated to cost of sales.

(g) Buildings are depreciated at 5% per annum on their original cost, allocated 30% to cost of sales, 30% to distribution costs and 40% to administrative expenses.

(h) Income tax has been calculated as $45,000 for the year.

【论述题】

The statement of profit or loss for the year ended 31 October 20X7