快速查题-ACCA英国注册会计师试题

ACCA英国注册会计师

筛选结果

共找出525题

- 不限题型

- 不定项选择题

- 单选题

- 填空题

- 材料题

- 简答题

- 论述题

This question appeared in the June 2015 exam.

X Co uses a throughput accounting system. Details of product A, per unit, are as follows:

Selling price $320

Material costs $80

Conversion costs $60

Time on bottleneck resource 6 minutes

What is the return per hour for product A?

The following data relate to a manufacturing company. At the beginning of August there was no inventory. During August 2,000 units of product X were produced, but only 1,750 units were sold. The financial data for product X August were as follows:

The value of inventory of X at 31 August using a throughput accounting approach is:

This objective test question contains a question type which will only appear in a computer-based exam, but this question provides valuable practice for all students whichever version of the exam they are taking.

Skye Limited has a two process environment, and details of these processes are as follows:

Process P: Each machine produces 6 units an hour and Skye has 8 machines working at 90% capacity.

Process Q: Each machine produces 9 units per hour and Skye has 6 machines working at 85% capacity.

One of Skye products is Cloud. Cloud is not particularly popular but does sell at a selling price of $20 although discounts of 15% apply. Material costs are $5 and direct labour costs are double the material cost. Cloud spends 0.2 hours in process P but 0.3 hours in process Q.

What is Cloud’s throughput per hour in its bottleneck process?

A company has recently adopted throughput accounting as a performance measuring tool. Its results for the last month are shown below.

Units produced 1,150

Units sold 800

Materials purchased 900 kg costing $13,000

Opening material inventory used 450 kg costing $7,250

Labour costs $6,900 Overheads $4,650

Sales price $35

There was no opening inventory of finished goods or closing inventory of materials.

What is the throughput accounting ratio for this product?

The following details relate to three services offered by DSF.

All three services use the same direct labour, but in different quantities.

All three services use the same direct labour, but in different quantities.

In a period when the labour used on these services is in short supply, the most and least profitable use of the labour is:

The following statements have been made about life cycle costing:

(1) Clean up costs should be included when assessing the profitability of a product

(2) It is useful for organisations that develop products with a relatively short life

Which of the above statements is/are correct?

This objective test question contains a question type which will only appear in a computer-based exam, but this question provides valuable practice for all students whichever version of the exam they are taking.

While a drag and drop style question is impossible to fully replicate within a paper based medium, some questions of this style have been included for completeness.

Which of the following are said to be benefits of lifecycle costing?

It provides the true financial cost of a product

The length of the lifecycle can be shortened

Expensive errors can be avoided in that potentially failing products can be avoided

Lower costs can be achieved earlier by designing out costs

Better selling prices can be set

Decline stages of the lifecycle can be avoided

Drag the items selected into the box below:

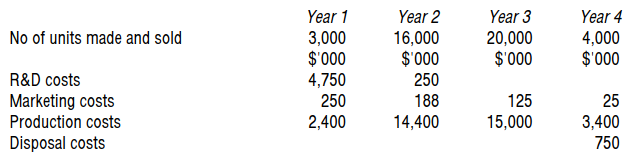

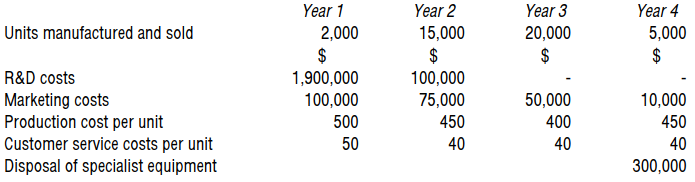

Moonface is developing a new piece of technology with the following expected costs.

What is the life cycle cost per unit?

材料全屏

14

【论述题】

Calculate the cost per unit looking at the whole life cycle and comment on the suggested price.

A manufacturing company uses three processes to make its two products, X and Y. The time available on the three processes is reduced because of the need for preventative maintenance and rest breaks.

The table below details the process times per product and daily time available:

Process Hours available Hours required to make Hours required to make

per day one unit of product X one unit of product Y

1 22 1.00 0.75

2 22 0.75 1.00

3 18 1.00 0.50

Daily demand for product X and product Y is 10 units and 16 units respectively.

Which of the following will improve throughput?

© 2024-2026 koolearn.com 版权所有 全国客服专线:400-676-2300

京ICP备2024050960号-2

京公网安备11010802044296号

ICP许可证编号:京B2-20241156

京公网安备11010802044296号

ICP许可证编号:京B2-20241156

![]() 新东方教育科技集团旗下成员公司

新东方教育科技集团旗下成员公司